Hello knowledge workers,

I am a firm believer of this philosophy “earning comes along with (l)earning” atleast in a knowledge economy ( offcourse there are few exceptions, what say you, Kannappan :-) The coincidental connotation (not sure if it was coincidental or intentional) of these words (learning and earning) had intrigued me right from my childhood.

Nevertheless, I feel that there is a strong relationship between earning and learning in an industry such as share market. So, let’s take the first step towards earning which is learning.

Numbers don’t lie though people who give out these numbers may lieJ. In my opinion numbers (or) metrics helps us in different levels based on the need of the hour.

Level 1 – Understand an “object of study” better.

Level 2 – Evaluate if it is good or bad

Level 3 – Compare (both 1 & 2 are in its absolute sense) whereas level 3 is in a “relative sense”

Level 4 – Predict (In this level we all tend to feel as if we were astrologers).

Note: Sometimes it is very difficult to understand the thin line of difference between 2& 3. So for all practical purposes we could consider level 2& 3 to be the same.

Let’s see how these 4 levels works while we make an investment decision in share market.

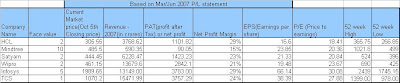

Here are the stats for some of the most renowned IT companies that I had considered for my investment options.

Here is the definition for each of these metrics…

Face Value à Par value (or) stated value of the share. This is not an important metric when you want to understand the intrinsic value (and) market value of the share. However this is an important number when you want to understand how dividends are given out every year.

Current Market price: The current price at which a share is traded.

Revenue: Overall sales of the company

PAT: Profit after tax in other words net profit

Net profit Margin: Revenue/PAT say for eg., for HCL it is 1101.82/3768.62 which is 29%

EPS: Net Income/Number of outstanding shares (for the definition of outstanding shares refer to the earlier installment)

P/E ratio: Current traded price/ EPS say for eg., for HCL it is 305.55/16.6 which is 18.41.

52 week high and low à should be self explanatory

In my opinion the key numbers that are to be used while making an investment decision are EPS (the higher the better it is) and P/E (the lower the better it is). The best metric that could give us an indication regarding the intrinsic value of the share (and also to understand whether a stock is trading at a much higher price than it is ought to be) is this P/E.

Let me not spoon feed you too much… let your thoughts take wings... Look at these numbers for any stock where you want to invest money. Streamline your thinking based on the four levels explained above. Make a choice. I am sure that the chances of repenting later will be greatly reduced if we all understand the implications of these numbers (not to mention that it is our responsibility to ensure that these numbers are correct).

Even to buy a t-shirt @ 150 rs. We ask fundamental questions such as,

- Is it worth buying at this price?

- Is there any other shop where I could buy this @ a cheaper price?

- Is there any shop where I could buy it @ a discounted price (say end of season sale)

Even to buy a product that is @ a price of 100 rs. We ask ourselves all these basic questions. Seldom do we ask the same questions while investing thousands of rs. in shares which is something that I had always failed to understand. Most often that not we tend to get carried away with the typical herd mentality...So, let’s get our basics right.

Have a nice weekend and many thanks for your patient reading,

Kiru.

{kind=link}